Dec 23 2024 1 mins 1

Welcome back to the ROI Club,

In my previous article I wrote:

Land is the longest-lived business asset and (along with water) probably the only perpetuity business asset that’s inflation-benefitting over the fullness of time.

The most valuable land on planet earth is arguably the Permian Basin, which covers 75,000 square miles mainly across Texas and New Mexico and boasts an estimated 100 billion Barrels of oil reserves.

In today’s piece, I’m adding in the other perpetual asset that’s truly an inflation beneficiary, providing progressively higher use cases and boasting its own natural refresh rate; water.

Many argue that the production growth in the Permian basin is about to roll over and given the rapid decline rates typical to shale wells that may well be true.

However, it’s estimated that the region is likely to remain producing for a further 40-50 years albeit by tapping into lower grade acreage with. Given that I’m invested in this thesis via royalty and land owners, I’m really far less concerned with the extraction economics as I don’t participate in that like I would if I were invested in an E&P (Explorer & Producer). I will benefit from any activity on the acreage I own via leases, royalties and possibly the most lucrative thing that almost no one is talking about, water handling fees.

Water has become such a large business in the oilfield that it now has its own conferences. You see, you really ought to understand this:

Fracking involves using vast amounts of water (sourced water) to extract oil and gas. For every barrel of oil produced, 3-5 barrels of non-potable water emerges and must be disposed (produced water). This is known in the industry as the water-cut.

Now, as activity increases in the Permian in an attempt to maintain the level of output which has powered the world since the shale revolution, ask yourself - what’s the bottleneck to production?

Water.

Not just the sourced water to frack, but the biggest menace is probably the produced water that emerges to the surface as a result and must be disposed of correctly.

My take is that more and more water will be produced because the easiest acreage has already been drilled. In other words, the water cut almost certainly increases over time and the costs of its handling will also rise.

My favourite children $TPL and $LB are my preferred way to gain exposure to this as the water-handling companies building the necessary pipeline to transport the water pay them easement fees for the right to traverse their lands. They also receive a royalty for every barrel that flows through said pipes

But what about the water handling companies themselves? You may ask - Surely they are worth a look?

Indeed they are and today I’m taking you through my latest new stock purchase.

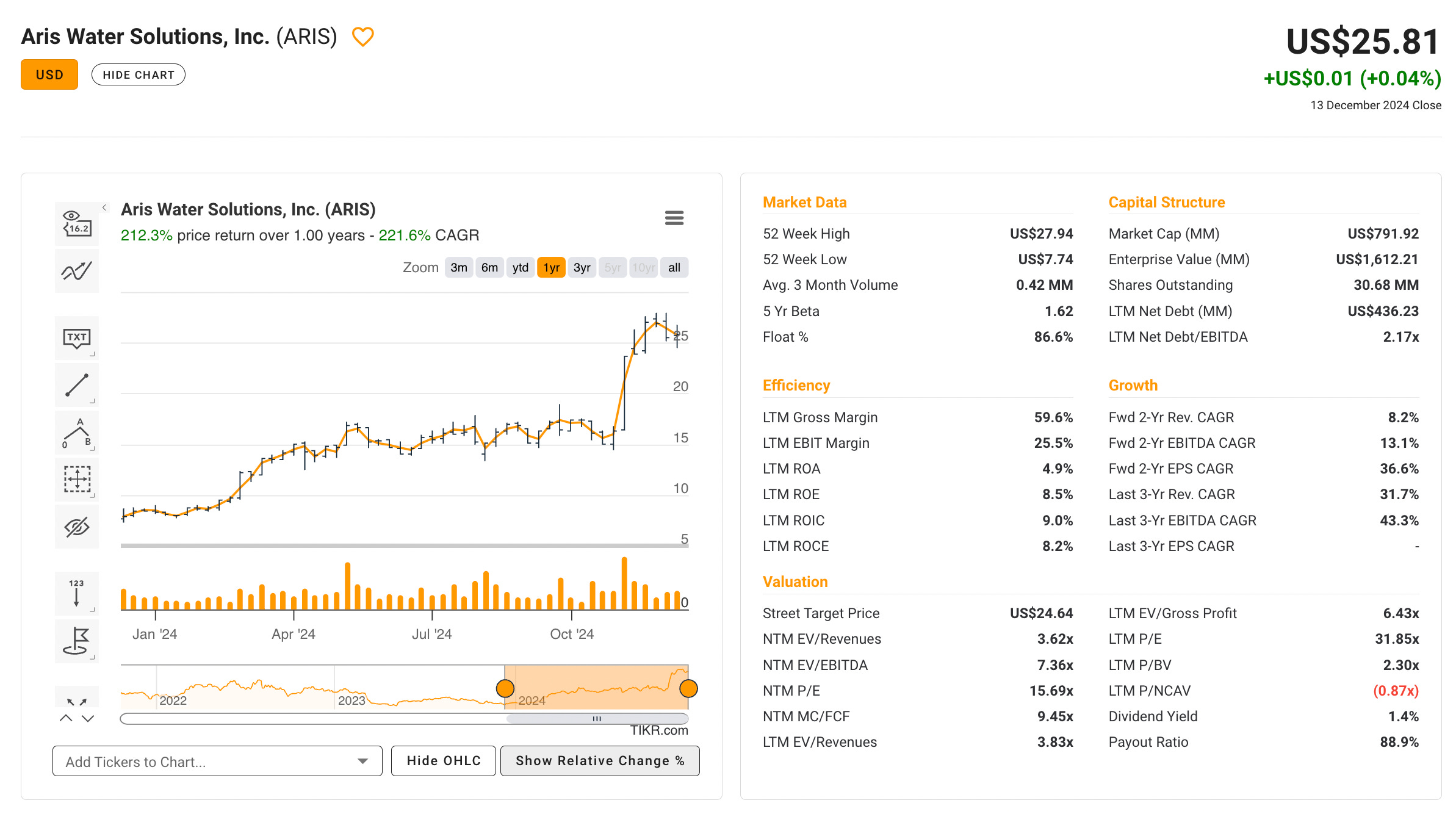

The stock I’m buying owns 775 miles of pipeline with a capacity to handle 1.8 million of these water barrels per day plus a rapidly growing water recycling and treatment segment. It holds long term contracts with the biggest producing oil companies in America who pay them to handle their water needs.

In its short 4 year history it has grown revenues at 25% CAGR, requiring no growth in CAPEX with constantly impressive margins.

It’s my contention that this company will grow even faster over the next decade, requiring no growth in capex as supported by their now starting to distribute cash via dividends.

Additionally, I estimate the stock is trading at circa 4x its 2024 EBITDA (E).

If you’d like to learn about a company who earns growing fees on 1.8 Million barrels of water which pass through its pipes every, single, day, then join the ROI club below. Where you’ll gain full access to all of my best ideas, many of which have already multi-bagged since I began publishing.

See you in the club.

Benjamin